Inventorying your entire lease portfolio to ensure compliance with FASB ASC 842 is potentially more challenging than you might suspect.

While you likely have a good handle on your real estate leases, do you have a true sense of all your equipment leases, or those sneaky embedded leases? Do you even know where all types of leases reside across your organization?

In what follows, we’ll provide some ways to help you ferret out all the leases impacted by the new accounting standards.

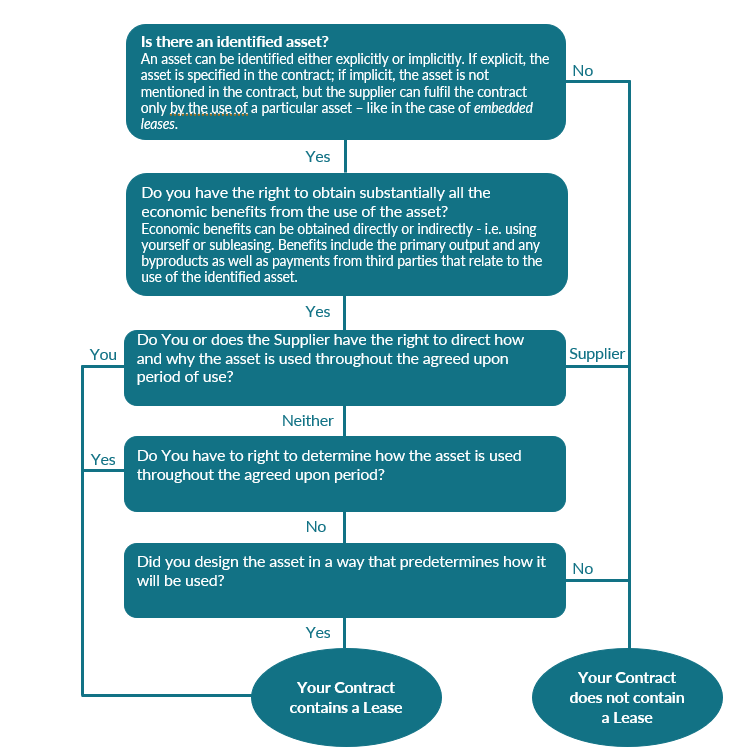

How Do You Define A Lease Under the New Standard? What is involved in control?

First, let’s agree on how a lease is defined under the new FASB ASC 842 lease standard: “A lease is an arrangement that conveys the right to control the use of an identified asset for a period of time in exchange for consideration.” This definition has two key points: control and identified asset.

One: The right to obtain substantially all the economic benefits from use of the identified asset.

Two: The right to control the use of the identified asset – to direct its use over the term of the lease.

What is meant by an identified asset?

It’s something that could be either implicitly or explicitly identified in a contract and can be a physically distinct portion of a larger asset. If the supplier has a substantive substitution right, the contract isn’t a lease. A supplier has the substantive right to substitute an asset if it both:

- Has the practical ability to substitute the identified asset

- Can benefit from exercising that right of substitution

The new FASB ASC 842 standard applies to property, plant and equipment leases, but does not apply to leases of intangible assets (i.e. goodwill, patents, trademarks and copyrights), leases to explore for or use non-regenerative resources, leases of biological assets, leases of inventory or leases of assets under construction.

Now that we understand what qualifies as a lease, you need tools to help uncover the leases that may exist across your entire organization. This step involves reaching out to various departments, regional offices, and any other locations within your enterprise where leases are likely hiding.

The question is, how do you help these individuals determine if they have leases that are subject to the new standards?

We recommend conducting interviews that follow a decision tree.

Leverage this Decision Tree to Determine Which Leases Qualify Under the New FASB ASC 842 Standards